What is Insurtech?

You might have already come across the term insurtech and know what it means but for those of you still unfamiliar with this emerging trend here is the meaning behind it – Insurtech comes from insurance and technology. Insurtech is also a subset of fintech, or financial technology. To put it simply, fintech as a whole disrupts the way we operate in the financial services, think of automated investment apps, instant online banking, crowdfunding platforms etc. Its narrower branch insurtech specializes in making client’s experience of insurance services convenient, easy and fast like never before, e.g online policy handling, automated accident processing tools, smartphone apps for instant access to valuable personal insurance data etc.

Essentially, insurtech can be understood as a new business model revolving around cutting-edge technology like ArtificialI Intelligence (AI), Big Data & the Internet of Things (IoT). My experience working in a bespoke software development company gave me valuable lessons on the importance of innovation. The IT industry with its innovative software solutions is a driving force for a positive impact on the world. Technology does not only make our lives easier, it is now so intertwined in our daily lives that it is sometimes unimaginable what the modern world would have looked like if it did not exist. Fortunately, our generation is lucky enough to be able to fully benefit from the digital era, so let’s see how the insurtech is going to change the game for the insurance sector

How does it work?

By now you probably have an idea how insurtech can make your life more convenient. Maybe you have even tried some app for personal insurance and were positively surprised just how easy the mundane task of filling out insurance policies or claiming damage can be. As they are relatively new, insurtech services rely on modern technologies to provide improved and customized consumer experience. To achieve this, insurtech streamlines and enhances backend processes, which is also cost-effective for insurtech vendors.

For instance, a streamlined process are virtual assistants and chatbots, who are reachable 24/7 to automatically provide the customer with answers to their insurance inquiries. Another example here are mobile apps, allowing clients to take a picture of essential documents and then instantly submit it for review, which is usually a lot faster than what we are used to in traditional insurance. Additional features let the app get to know your preferences and offer you individually customized offers that fit your needs without going to the office personally.

Emerging Technologies in The Sector

Internet of Things

Internet of Things or the common abbreviation IoT is an emerging technology that gained popularity in the last years. IoT connects different devices or ordinary machines in a network, where they can transmit data between one another. This way of communication is based on embedded sensors, custom software and special system architecture with automated protocols. Insurtech can benefit from IoT in multiple ways.

Imagine a person rents a car that uses telematics to collect, store and transmit data about the driver’s behaviour (speed, acceleration, exact location etc.) via wireless internet. Insurance providers can observe individual driving patterns and if those are responsible they can offer discounts on insurance services. Similar use case is found with wearables such as smartwatches – they can collect personal data to analyze individual risks to be able to make a tailor made offer based on a person’s habits and activity.

Machine Learning

Machine learning (ML) is a subset of AI and it trains machines to learn over time given that enough and relevant data is provided. Machine learning in insurtech can be very useful as it gives invaluable insights on individual behaviour patterns, something traditional insurers may find hard to obtain. Based on collected data, ML can generate accurate prediction models about customer’s individual actions to create customized solutions without missing important details.

One can say that ML helps insurers see the bigger picture, instead of just fragmented personal information.What is more, ML allows insurance providers to mine their data so the focus can stay on the relevant data needed. Some popular use cases here are e.g. risk modelling to predict potential future losses, demand forecasting to predict certain future demands, fraud detection, claim processing or underwriting.

Drones

Drones are particularly effective in the property insurance sector. Due to extreme weather conditions or hazardous substances sometimes it might be impossible to use manforce to inspect property damages and drones with their small size and mobility are an important asset in monitoring and inspection. In fact, insurers are early adopters of commercially applied drones estimated to save companies around 6.8 billions UDS per year. Specific areas where drones come handy are post disaster claim inspection, roof and boiler inspections and fraud monitoring. Moreover, drones can be employed in risk assessment to calculate certain risks before property is insured and also help in preventive maintenance in certain times of the year with increased disaster risks (e.g heavy storms or hurricane alerts).

Some of the numerous advantages of drones are that they help facilitate the claim management process by accelerating the time for damage assessment. It is estimated that drone employment

can boost the inspection efficiency by up to 85%. Needless to say that tech devices help improve the customer satisfaction – the quicker a damage is being documented and inspected, the quicker insurance can be paid to a policyholder.

Artificial Intelligence

As already discussed in a section above, AI can offer lots of benefits for insurance providers. AI algorithms enable higher degree of customization for a person. An AI-based insurance app can notice travel habits of a person who tends to travel near-distance and only on holidays. His or her individual risk is likely to be lower than that of someone who travels to remote places every two months, so the first person may receive discounted prices thanks to AI algorithms.

After being fed relevant data and trained properly, AI gets proficient in image recognition and

can be effectively used for better image analysis regarding complex decisions where a single mistake can cost large amounts of money for insurers. Capturing various parameters AI can also model competitive pricing options for different insurance businesses so that customers can choose the right option for themselves based.

Recommended Reading :

- Artificial Intelligence & Machine Learning in E-Commerce

- Can Artificial Intelligence Replace Human Intelligence?

- Artificial Intelligence and How it Can Improve your Customer Support

Blockchain

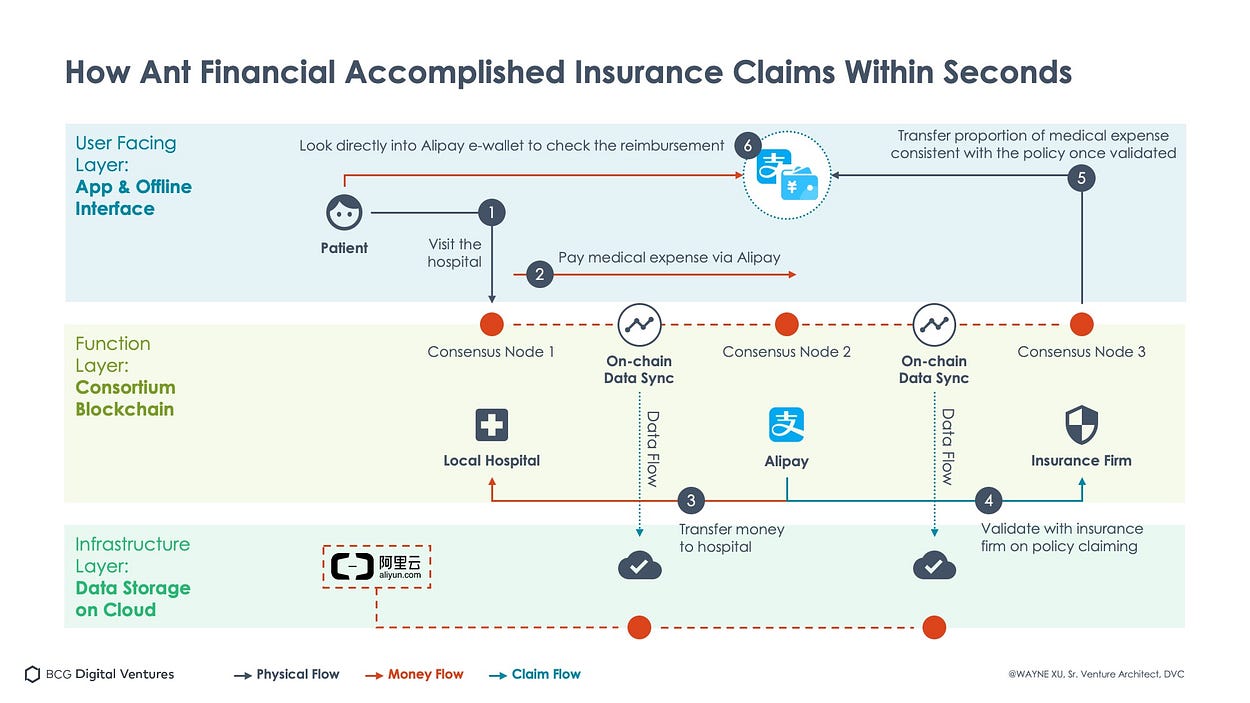

If your only association with blockchain is cryptocurrency, you might be surprised that this type of records (blocks) linked via cryptography can also be used in insurance. Blockchain technology is successfully applied for fraud prevention to detect malicious or illegal actions. This is achieved because blockchains are developed by design to be resistant to data modification.

This infographic shows a visual representation of just how blockchain models operate and what is the blockchain’s path through different layers. Within seconds after paying their medical expenses via an app, on chain data synchronises with and flows to the cloud and the insurance firm receives validation for policy claims. Huge investments are made in research on how to further improve this technology and to expand its applications. All these steps reduce transaction costs, help to lower potential credibility frictions as well as enhance liquidity on transferable policies and assets.

How Is It Changing The Insurance Sector?

The following three features of insurtech are considered top reasons why insurtech might disrupt this traditional industry:

Risk Analysis

From all discussed above, it is clear that insurtech is on its way to change how insurers analyse risks. With a strong arsenal of powerful technologies such as AI, ML or drones becoming increasingly used, it will soon be unthinkable for the insurance sector not to have technology on their side. Let’s face it, risk analysis is an essential step for all insurance services and risk predictability algorithms provided from smart AI technologies and big data analysis on consumer behaviours are now key to successfully make sense of the huge amounts of data available.

On-Demand Services

What is probably one of the most important attractive features of insurtechs is that they offer on-demand services with instant access to just what clients need. Going away for the weekend? Borrowing a friend’s car? Insurtech customers will be offered the right insurance service whenever they want and for as long as they need it. Think of the freedom and satisfaction this gives the end-user.

Personalization and Customized services

Another way insurtech disrupts traditional insurance businesses is by making unique and tailor made offers to their customers. Each individual preferences, habits and involved risks are taked into consideration by intelligent technologies at the backend so that a personalized insurance policy can be created that fits exactly the needs of a person.

To sum it up, on one hand, all innovative applications of technology mentioned today have the potential to disrupt the traditional insurance sector. if those do not come to terms with new tech capabilities, they may risk staying behind on their own territory. On the other hand, insurtechs as new players may still sound too unfamiliar for the clients, so a strategic partnership connecting tradition with innovation, the best of both worlds, may be just what end-consumers need to be satisfied. It is clear though how much convenience insurtech can offer and how beneficial it can be for both companies and policy holders.

{kind=link}

{kind=link}